Pay Yourself First: The One Rule That Builds Wealth

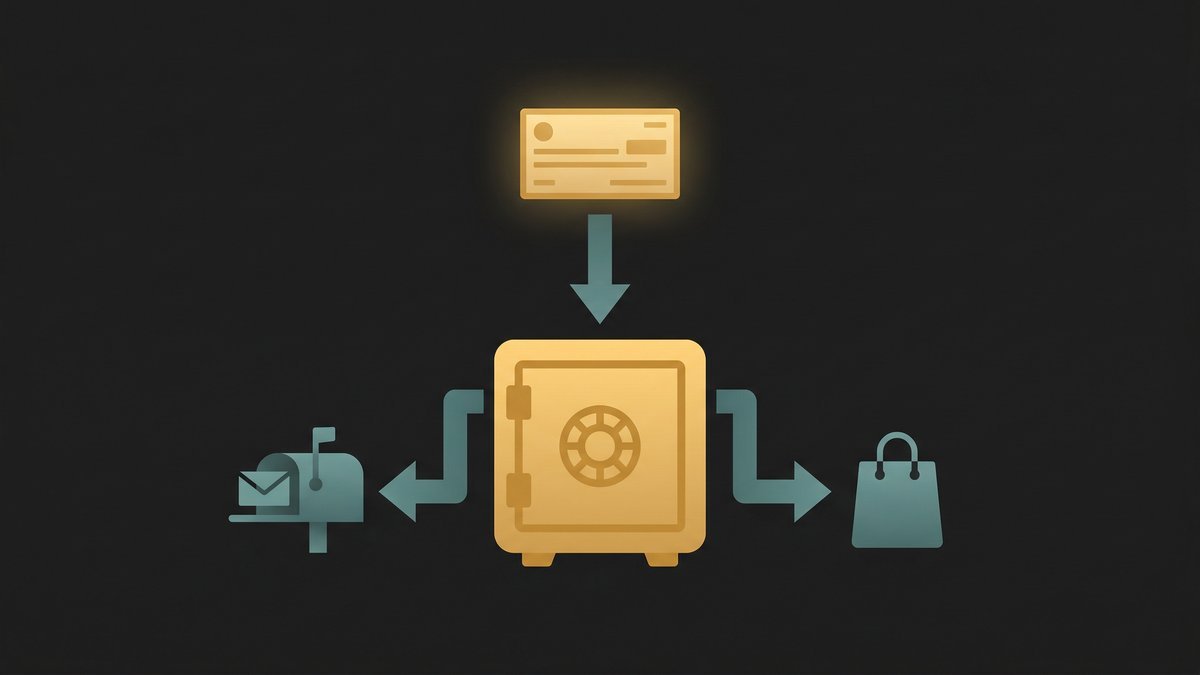

The pay yourself first rule is the simplest behavioral change in personal finance — and arguably the most powerful. The concept: when your paycheck arrives, the very first thing that happens is money moves into savings and investments. Not after bills. Not after discretionary spending. Not after you’ve “seen what’s left.” First. Before anything else touches it.

Most people do the opposite. They earn money, pay their bills, spend on daily life, and then try to save whatever survives. The problem is that “whatever survives” is usually close to nothing. Expenses expand to fill available income — a phenomenon so reliable that economists named it Parkinson’s Law of Money. If the money is in your checking account, it gets spent.

The pay yourself first strategy reverses this default. It treats savings and investing as the first “bill” — one that gets paid automatically, on the same day as your paycheck, before you make a single spending decision. According to Fidelity’s 2025 retirement analysis, people who automate their savings using a pay yourself first approach save 3–4 times more consistently than those who save manually at the end of the month. Not because they earn more — but because the system removes the decision.

What Does Pay Yourself First Mean?

Pay yourself first means directing a predetermined portion of your income — typically 15–20% — into savings and investment accounts the moment you get paid. It’s called “paying yourself” because the money goes toward your future wealth, not toward someone else’s business (rent, utilities, subscriptions).

The sequence looks like this:

- Paycheck arrives.

- Automated transfers fire immediately: savings, investments, debt payments above minimums — all pre-scheduled for the day after payday.

- Bills get paid (most on autopay).

- Whatever remains in your checking account is your guilt-free spending money for the pay period.

Compare that to the conventional approach:

- Paycheck arrives.

- Bills get paid.

- Spending happens throughout the month.

- At the end of the month, you check the balance and try to save whatever’s left (usually $0–$100).

Same income. Same expenses. Radically different outcomes — because the order changed. When you pay yourself first, savings happens by default. When you save last, it happens by accident (or not at all).

Why Pay Yourself First Actually Works

The pay yourself first strategy succeeds because it aligns with how human behavior actually operates — not how we wish it operated.

It Eliminates Decision Fatigue

Every manual savings decision is a negotiation: “Should I save this money or use it for something else?” After a long day, when your car needs new tires or a friend invites you to dinner, the “something else” almost always wins. The pay yourself first approach removes the negotiation entirely. The money is gone before you can debate it.

It Leverages Loss Aversion

Psychologically, losing something you already have feels worse than not gaining something new. When savings happens first and your checking account shows a lower “available” balance, your spending naturally adjusts downward — without requiring a detailed budget. You spend based on what’s visible, and your savings are already invisible (in a separate account at a separate bank).

It Creates a Forced Constraint

Most people who say “I can’t afford to save” actually mean “I spend everything I earn before I get around to saving.” The pay yourself first strategy proves that you can afford it — by making the adjustment upfront and finding that daily life adapts. Within 2–3 months of automatically saving 15% of your paycheck, you stop noticing the difference in your spending. The constraint becomes your new normal.

How to Pay Yourself First: The Setup

The pay yourself first system takes about 30 minutes to set up and requires no ongoing maintenance beyond a quarterly check-in. Here’s the implementation:

1. Decide Your Percentage

The standard target is 20% of after-tax income (the savings portion of the 50/30/20 budget rule). If that’s too aggressive to start, begin with 10% and increase by 1–2% every quarter until you reach 20%. The key is that the percentage is non-negotiable — it’s a fixed commitment, not a suggestion.

On a $4,000/month take-home pay:

- 10% = $400/month paid to yourself first

- 15% = $600/month

- 20% = $800/month

2. Decide Where It Goes

Your “pay yourself first” money should flow into accounts based on your current financial priorities. Here’s the typical allocation sequence:

- If you don’t have an emergency fund: 100% to a high-yield savings account until you reach $1,000–$2,000.

- If you have high-interest debt: Split between emergency fund (minimum) and aggressive debt payoff.

- If the foundation is solid: Direct most of it into investing — Roth IRA, 401(k) beyond the match, or a taxable brokerage account in low-cost index funds.

You can split the pay yourself first amount across multiple goals — for example, $300 to Roth IRA, $200 to emergency fund, $100 to extra debt payments. The destinations change as your priorities shift. The habit of paying yourself first stays constant.

3. Automate It Completely

This is what makes the pay yourself first system work over the long term. Set up automatic transfers scheduled for the day after payday:

- Checking → High-yield savings (emergency fund / short-term goals)

- Checking → Brokerage or Roth IRA (investing via dollar-cost averaging)

- Payroll → 401(k) (deducted before the paycheck even reaches your account)

The 401(k) is the purest form of pay yourself first — the money is deducted from your paycheck before you ever see it. You literally can’t spend it because it never enters your checking account. Every other automated transfer replicates this effect for your other financial goals.

4. Spend Everything That’s Left — Guilt-Free

This is the part most financial advice leaves out. Once you’ve paid yourself first and your bills are covered, the remaining money in your checking account is genuinely yours to spend. On anything. No tracking required. No guilt.

Want to eat out? Fine — savings is already handled. Want new shoes? Fine — your investments already fired this morning. The pay yourself first approach doesn’t eliminate enjoyment. It sequences it correctly: build wealth first, spend freely second.

This is why the strategy is sometimes called “reverse budgeting” — instead of budgeting every category and hoping savings happen at the end, you save first and let spending fill whatever’s left. It’s a fundamentally less stressful way to manage money.

A Real-World Example: Two Paychecks, Two Systems

Luis and Hana are coworkers, both 30, both earning $58,000 ($3,800/month take-home). Both have similar expenses: rent, car payment, groceries, insurance, subscriptions. Their financial lives look identical on paper — except for one difference.

Luis saves last. He pays his bills, lives his life, and transfers whatever is left in his checking account to savings at the end of each month. Some months it’s $200. Some months it’s $50. Most months, it’s nothing — because something always comes up.

Hana pays herself first. On the day after payday, $760 (20% of take-home) is automatically split: $400 to her Roth IRA invested in VTI, $200 to her high-yield savings, and $160 to extra student loan payments. She never sees this money in her checking account. She spends whatever’s left — roughly the same amount Luis spends — without guilt or tracking.

After 5 years:

- Luis: ~$4,200 in savings. Inconsistent deposits over 60 months, averaging about $70/month when he remembers.

- Hana: ~$31,500 in her Roth IRA (contributions + compound growth), $12,000 in high-yield savings, and $9,600 in extra student loan payments made. Total financial progress: ~$53,100.

Same salary. Same city. Same lifestyle. Hana has $53,100 in financial assets because she automated a pay yourself first system in her mid-twenties. Luis has $4,200 because he relied on willpower and end-of-month leftovers. The income wasn’t the variable. The sequence was.

The Pay Yourself First Percentage Ladder

If jumping to 20% feels overwhelming, use a percentage ladder — start low and ratchet up on a fixed schedule:

- Month 1–3: Pay yourself first at 5% of take-home

- Month 4–6: Increase to 8%

- Month 7–9: Increase to 12%

- Month 10–12: Increase to 15%

- Year 2: Reach and hold at 20%

Each increase is small enough that your daily spending barely adjusts. By the time you reach 20%, the habit is locked in and you’ve been living on 80% of your income for months — without feeling deprived.

The most powerful version of this: every time you get a raise, increase your pay yourself first percentage by half the raise amount. If you get a $200/month raise, increase your automated savings by $100. You still experience a $100 lifestyle improvement, but your savings rate climbs with every raise — eventually reaching 25%, 30%, or more.

Pay Yourself First vs. Traditional Budgeting

Traditional budgeting asks you to control dozens of spending categories: $400 for groceries, $150 for dining, $80 for entertainment, $50 for subscriptions. It works for people who enjoy tracking — but most people find it exhausting and abandon it within months.

The pay yourself first approach only requires you to control one number: your savings percentage. Everything else — groceries, dining, entertainment, gas — comes out of whatever remains. You don’t track categories. You don’t agonize over a $7 latte. The only decision that matters is: “Did I pay myself first today?”

Both methods work. But for people who have tried and abandoned detailed budgeting (which is most people), the pay yourself first method is dramatically more sustainable. It works because it asks less of you — and less is exactly what makes financial systems stick over decades. The 50/30/20 rule is essentially a structured version of pay yourself first: the 20% savings portion is the “pay yourself first” allocation, and the remaining 80% is divided between needs and wants without micro-tracking.

Common Objections to Pay Yourself First

“I can’t afford to save right now.”

Start at 5% — even 3%. On $3,000/month take-home, 3% is $90. If you genuinely cannot redirect $90 per month, you have an income or expense problem that needs addressing before any financial strategy will work. But for most people, $90 can be found by canceling one or two unused subscriptions. Start small. The habit matters more than the amount.

“What if I need that money for bills?”

If your essential bills consume 100% of your income, the pay yourself first percentage needs to be smaller initially — but it should still exist. Even $25 per paycheck into a separate emergency savings account creates a buffer that prevents the next unexpected expense from going onto a credit card. Simultaneously, look for ways to increase the gap between income and expenses: negotiate bills, eliminate subscriptions, or add a side income stream.

“What if I set the percentage too high and overdraft?”

Start conservatively and monitor for 2–3 months before increasing. If the first month is tight, reduce by 2% and stabilize. The percentage ladder approach prevents this problem — you start well below your capacity and ratchet up gradually. Better to save 8% consistently for a year than to save 20% for one month and then stop because it was unsustainable.

Frequently Asked Questions

What does pay yourself first mean?

Pay yourself first means automatically directing a portion of your income into savings and investments the moment your paycheck arrives — before paying bills, before discretionary spending, and before you have a chance to spend it elsewhere. It’s the practice of treating savings as your first financial obligation, not your last. The concept was popularized by personal finance authors George Clason (The Richest Man in Babylon) and David Bach (The Automatic Millionaire).

How much should I pay myself first?

The standard recommendation is 20% of after-tax income. If that’s not feasible right now, start with 10% — or even 5% — and increase by 1–2% every quarter until you reach your target. The habit of paying yourself first at any percentage is more valuable than waiting until you can afford 20%. Consistency matters more than the specific amount at the beginning.

Is pay yourself first the same as budgeting?

Not exactly. Traditional budgeting assigns every dollar to a specific category and tracks spending in detail. Pay yourself first (sometimes called “reverse budgeting”) only requires one decision: how much to save before spending. Everything else is flexible. Many people use pay yourself first as a simpler alternative to detailed budgeting — or combine it with a framework like the 50/30/20 rule for additional structure without granular tracking.

The Bottom Line

The pay yourself first principle is the behavioral foundation beneath every other financial strategy on this site. Financial goals, automation, index fund investing, net worth growth — all of them require one thing: money directed toward your future before it’s absorbed by your present. That’s all “pay yourself first” means.

Set a percentage. Automate the transfer. Spend what’s left without guilt. Review quarterly. Increase the percentage with every raise. That’s the system — and it’s been quietly building wealth for disciplined savers since long before anyone called it a “strategy.”

The people who build wealth aren’t the ones who earn the most. They’re the ones who keep the most — because they pay themselves before they pay everyone else.

This article is for educational and informational purposes only. It does not constitute personalized financial or investment advice. Always consult a qualified financial professional before making financial decisions.

Ready to build the system? The Money Mechanics Playbook covers all the fundamentals – from your first budget to your first investment. Get the free playbook here.